What’s Happening in Lentil Markets?

Just a few weeks ago, there was a lot of “excitement” in the lentil market. The government in India, the world’s largest lentil buyer, had proposed a couple of restrictions on imports that caused considerable concern. Since then, both of the threatened trade restrictions have been withdrawn, at least temporarily, and the market has returned to normal.

Truth be told, there was no measurable slowdown in Canadian lentil trade. Even before the Indian government back off from its proposed import barriers, volumes of lentils delivered by Canadian farmers and shipped out by country elevators had turned higher, well above normal levels for this time of year. Exporters had already figured out how to work around the proposed restrictions, and that allowed the market to stabilize.

While these trade issues triggered a slide in Canadian prices, it caused a bounce in Indian lentil prices as buyers there were concerned about availability of lentils. Since then, that mini-rally has run out of steam, with green lentil prices in India mostly levelling off while red lentils dipped again. One factor keeping red lentil prices under pressure is the heavy pace of Australian exports after its record 2016/17 crop.

It’s worth noting though that India hasn’t been the be-all and end-all for the lentil market this year. Up to the end of January, lentil imports in India’s 2016/17 marketing year (Apr/Mar) have actually trailed last year’s pace significantly. For Apr-Jan, India had imported 620,000 tonnes compared to 1.13 million tonnes the previous year. Fortunately for Canada, Bangladesh and Pakistan have boosted their imports, helped by more affordable prices. Turkish demand has also been solid, although it will soon harvest its own lentil crop.

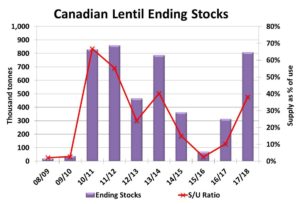

Despite a solid export year, Canadian lentil ending stocks for 2016/17 will be fairly large again, estimated at 430,000 tonnes. Most of those lentils however will be #3 or lower quality, which means supplies of #2 or better will actually be very tight going into 2017/18.

Of course, the big question is how many acres Canadian farmers will plant this year. Most analysts are expecting fewer acres due to concerns from last year’s disease problems. StatsCan’s planting intentions report will be the first survey-based estimate but won’t be the final word yet. And the eventual yield will play an equally large role in determining the crop size and 2017/18 supplies.

We already know that US farmers are planning on planting record acreage of lentils, although most of those will be medium greens and will have less effect on the red lentil market. We’re also hearing rumblings that farmers in other countries are looking favourably at pulses. Kazakhstan is one of those places where increased competition could start showing up.

Mid-April is still the very early stage of determining the 2017/18 market outlook and lots will still change. The most optimistic signal for both the short-term and long-term outlook is that global and domestic demand for lentils (and other pulses) is still growing at a strong pace which means there will be large opportunities for Canadian lentil exports again next year.