Here are our three main takeaways from April’s export data:

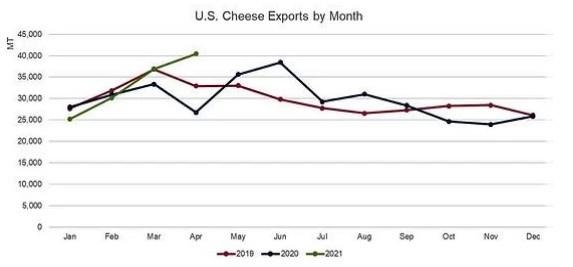

U.S. cheese resurgence

Towards the end of last year and into January of this year, U.S. cheese exports were sluggish due to weaker demand in Mexico alongside U.S. government purchases causing U.S. cheese to be priced well above the world market during the summer and fall of 2020. However, the past two months have shown that as government spending and price volatility waned over the winter and Mexico’s economy began to reopen, U.S. cheese exporters took advantage to book more export sales.

In April, U.S. cheese exports hit a record with gains spread across major markets. Shipments to Korea grew by 3,620 MT, Mexico by 3,056 MT, Central America by 1,799 MT, South America by 1,159 MT, Japan by 1,427 MT, Australia by 559 MT, and the list goes on. The gains in Latin America, especially Mexico and Central America, are perhaps the most encouraging, considering cheese demand in those markets was acutely hit by the COVID-19 pandemic, its economic effects and loss of international tourism. Increased exports indicate recovering demand in those markets as vaccine distribution accelerates and travel resumes.

Given that U.S. cheese production grew by 8% in April off strong milk production and new processing capacity, increased U.S. cheese exports for the month should not come as a surprise. With supplies generally available, international buyers clearly sought out affordable U.S. cheese, and the U.S. had the cheese to sell.

This dynamic provides further reason for optimism for U.S. cheese exports in the coming months as U.S. milk and cheese production continues to expand. Overall, with international demand accelerating and available product out of the U.S., we should continue to see strong cheese exports into the summer and early fall.

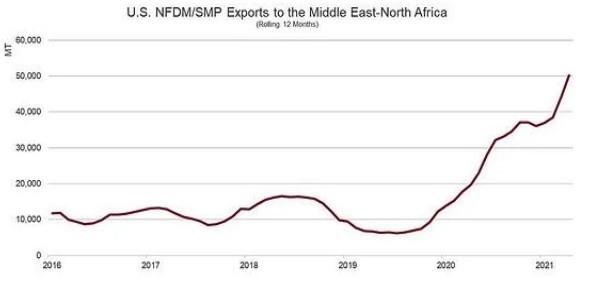

NFDM/SMP: Rebound in Mexico, slowdown in SEA

Cheese wasn’t the only major product category to grow. U.S. NFDM/SMP exports in April gained 16% (+10,500 MT) compared to April 2020, thanks to a strong rebound in exports to Mexico and new business in the Middle East/North Africa (MENA). Total NFDM/SMP shipments to Mexico grew by 43% (+8,052 MT).

Like cheese, NFDM/SMP demand in Mexico had been weaker over the past year due to the pandemic and the economic situation. April marks the third consecutive month of growth and points to greater demand within the country. Whether this increased demand persists largely depends on the cause.

In April, nearly 85% of Mexico was facing drought conditions, including its major milk-producing regions. This likely drove Mexican buyers to the international market for dairy products and inputs to ensure adequate supplies on hand, which has helped bolster U.S. exports. If the drought was the primary cause of the growth and not increased consumer demand, we could see a slowdown in shipments by June.

Thankfully, the U.S. has become increasingly diversified. Last year, the U.S. relied heavily on Southeast Asia (SEA) as an alternative destination. While volumes to SEA remain substantial, April shipments lagged 2020 volumes, falling 27% (-9,112 MT). Looking back, U.S. NFDM/SMP exports to SEA in April 2020 were the second highest on record. So, a decline in and of itself is not overly concerning. Still, port delays out of the West Coast remain a concern and have left some buyers frustrated with not being able to source product when they need it. Active communication about delays by U.S. exporters and improved port conditions will be essential to maintain market share in the region.

Instead, the U.S. shipped much greater volumes to MENA. In fact, the past two months posted the second and third highest NFDM/SMP export months of all time to the region (9,215 MT in March, 9,012 MT in April). This is relatively new business for U.S. exporters as the MENA region is the priority region for the European Union, so greater volumes here are particularly encouraging.

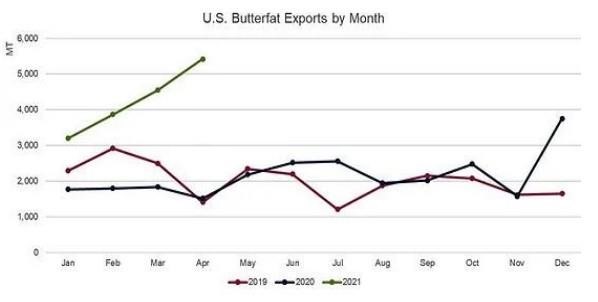

Butterfat exports booming

The United States may not boast the export volumes of the world’s dominant butterfat suppliers—New Zealand and the EU—but we haven’t seen this level of butterfat shipments since 2014. April butterfat exports jumped 257% (+3,904 MT) over the previous year, but this trend has persisted before April. U.S. shipments over the first four months of 2021 were 17,039 MT, an increase of 146%, or more than 10,000 MT.

A prolonged period of price competitiveness alongside strong demand from the Gulf Cooperation Council, assisted by the broader region’s ongoing efforts to diversify suppliers, have been the main drivers all year. U.S. butter exports to MENA grew 623% (+5,558 MT) over the first four months, compared to the same period in 2020.

Click here to see more...