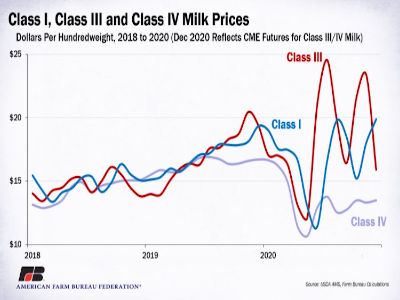

The price of Class III milk (milk used to produce cheese) rose to near-record highs in 2020 on the back of increased cheese demand, tighter cheese supplies and USDA’s Farmers to Families Food Box Program. Meanwhile, the price of Class IV milk (milk used to produce butter and dry milk powders) remained at multi-year lows due to COVID-19-related market disruptions and price volatility. As a result, the difference between the Class III milk price and other prices of milk rose to record-highs. In June, 2020, the Class III milk price was more than $9.60 per hundredweight higher than the base Class I milk price. Similarly, in July, the price difference between Class III and IV rose to nearly $11 per hundredweight.

Due to these record-large price spreads and a 2018 farm bill change to Class I milk pricing rules, record amounts of milk were de-pooled from Federal Milk Marketing Order revenue sharing pools and producer price differentials reached record-low levels in component pricing orders, e.g.,

De-Pooling and Record-Large Negative PPDs Continue Into July. Producers in primarily fluid milk marketing orders didn’t have negative PPDs, but experienced milk prices well below the levels they would have seen had the milk price not been modified in the 2018 farm bill, e.g.,

Impact of the Farm Bill Change to the Class I Milk Price on Dairy Farm Income. The financial impact of these issues has collectively cost dairy farm families across the U.S. more than $3 billion in foregone income.

With another Food Box-style program, many of these challenges would likely continue into 2021 as cheese prices would be mostly disconnected from the rest of the dairy industry. Without another Food Box-style program, the expectation is that the price spread between the four classes of milk will narrow in the coming months, reducing (but not likely eliminating) the negative PPD and de-pooling incentives. Today’s article reviews recent negative PPDs by FMMO, estimates the total value of negative PPDs on FMMO revenue sharing pools and identifies potential dairy policy options.

Negative PPDs in 2020

Negative PPDs occur when the component value of milk (value of butterfat, protein and other solids) in the FMMO pool exceeds the classified value of milk (value of milk as utilized) in the pool. In 2020, the component value of milk approached all-time highs due to the impact of the cheese price on the protein price. Then, because the higher-of was eliminated in the 2018 farm bill, the Class I price of milk did not entirely benefit from higher cheese prices. As a result, PPDs dropped to historic negatives and a significant volume of milk was de-pooled (making the PPD more negative).

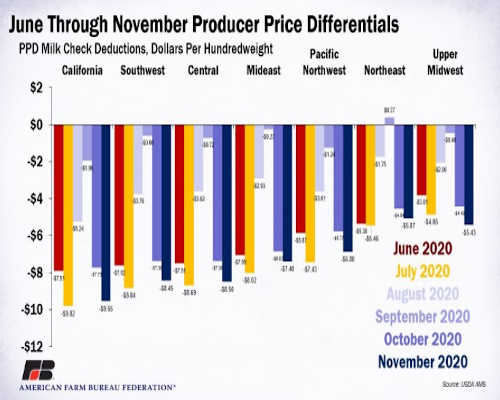

Recently announced statistical uniform prices for November 2020 reveal negative PPDs range from a low of -$9.55 per hundredweight in the California FMMO to a high of -$5.07 in the Northeast FMMO. From each principal pricing point, i.e., Cuyahoga County, Ohio, in the Mideast FMMO, PPDs are adjusted up or down based on the location adjustment in the county in which the farm is located (Background on Class I Differentials).

When combined across all FMMO component pricing orders, the total negative PPD reached a low of -$667 million in July, and recently reached -$619 million during November. Combined, the value of negative PPDs, i.e., the shortfall in FMMO revenue sharing pools, from June to November is estimated at -$2.7 billion. The impact of the negative PPDs will vary based on the volume of milk pooled on the FMMO and the utilization of milk pooled on the FMMO. When viewed by marketing area, the FMMO pools were the most deficient in California at -$774 million, followed by the Northeast at -$472 million.

Farm-Level Perspective

To put this into a farm-level perspective, assuming a national average milk yield per cow of nearly 12,000 pounds of milk produced from June to November, a 200-cow dairy in western Pennsylvania would have experienced PPD milk check “deductions” of nearly $130,000. Similarly, for a 3,000-cow dairy operation in California, the negative PPDs would represent milk check deductions of more than $2.5 million. What makes the situation even worse is public and private risk management tools such as Chicago Mercantile Exchange futures contracts, Dairy Margin Coverage and Dairy Revenue Protection were unable to protect against PPD price risk. Margin calls on Class III milk likely made the negative PPDs sting even more as milk prices rapidly rose.

The question many dairy industry stakeholders are asking is: “Where does that money go?” The answer is that the component value of the milk – in this case protein – was never in the pool in the first place. By mostly de-pooling Class III milk, the higher protein value was never part of the revenue sharing pool. Then, because Class I milk prices were well below Class III prices, the contribution to the FMMO pool from the beverage milk market was not enough to offset the component value of the milk.

The higher revenues associated with selling cheese or supplying a cheese plant were retained by the cheese manufacturer, the cooperative supplying the cheese plant, the cooperative manufacturing and selling cheese or the independent dairy farmer supplying a cheese plant. In many cases, dairy farmers in these situations may have been shielded from negative PPDs. Because only Class I milk is required to be in the pool, this is all well within the FMMO rules.

What Can Be Done?

There is no silver bullet fix to these issues. FMMOs, milk pricing provisions and pooling rules are complex.

Historically, because of advanced pricing there have always been scenarios in which the component value of milk exceeds the classified value of milk, resulting in de-pooling and negative PPDs. In the past it was somewhat contained by the higher-of, but that was eliminated in the 2018 farm bill. The higher-of was designed to ensure that fluid milk prices were always based on the maximum manufacturing value of milk used to produce cheese, butter and nonfat dry milk powder. By pricing milk based on the higher-of, the financial incentive generally existed to pool manufacturing milk on the FMMO because milk used for manufacturing purposes received proceeds from the higher-valued beverage milk market (see page 4 of USDA’s FMMO overview

here).

But, the higher-of prevented the effective use of CME futures contracts for Class III and IV milk to hedge Class I beverage milk, so going back to that is likely off the table. Other options include capping, or snubbing, the difference between the manufacturing values of milk when determining the Class I price; using a moving average of the difference in manufacturing milk classes in the Class I price formula, i.e., replacing 74 cents per hundredweight with a moving average differential; basing the Class I price on the value of Class III milk plus a fixed or moving average differential; or eliminating the advanced pricing nature of fluid milk with any combination of the aforementioned modifications (after all, you can now hedge the price in advance),

The level of complexity or simplicity varies with each alternative. Additionally, any approach utilizing a moving average differential or snubber will increase basis risk when hedging fluid milk. However, to the extent that any of these options increase the fluid milk price, negative PPDs and the incentive to de-pool would be reduced (not eliminated).

To address de-pooling, some have suggested stricter pooling requirements that make it more difficult to enter and exit the pool. However, most handlers likely appreciate that flexibility when it is financially beneficial to them. Some have floated the idea of mandatory pooling, but that likely goes beyond the original intent of FMMOs in regulating the fluid milk market. A proposal to address negative PPDs involves blending them into the component values. The PPDs would be there, but would be in the form of different prices for butterfat, protein and other solids in each FMMO. That would certainly complicate the use of risk management tools. (Mandatory pooling and blended component values were included in early proposals for the California FMMO).