By James Mitchell

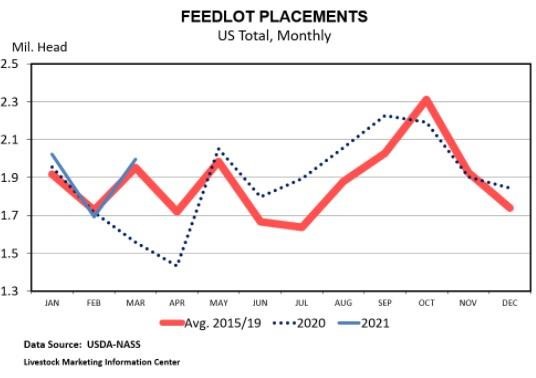

Last month Kenny, Josh, and I wrote about the challenges with making year-over-year comparisons to 2020. Comparisons will be based on periods in 2020 when COVID was having major impacts on the beef sector. Last week’s highly anticipated Cattle on Feed report was the example we had in mind when we wrote that article. The Cattle on Feed (COF) report includes estimates for feedlot placements, inventory, and marketings, and each was hard to predict.

The graph above shows feedlot placements for 2021 (blue line), 2020 (dotted blue line), and the 2015-2019 average (red line). March feedlot placements totaled 1.997 million head, a 28.3 percent increase over March 2020. The cattle placement estimate is a product of two events. First, recall this time last year was when the pandemic started impacting U.S. meat supply chains. This explains why placements are large compared to the previous year. Second, 2021 March placements are likely elevated on delayed placements from February due to Winter Storm Uri. While the March placement figure seems large compared to 2020, it is only 2.4 percent above the 2015-2019 historical average.