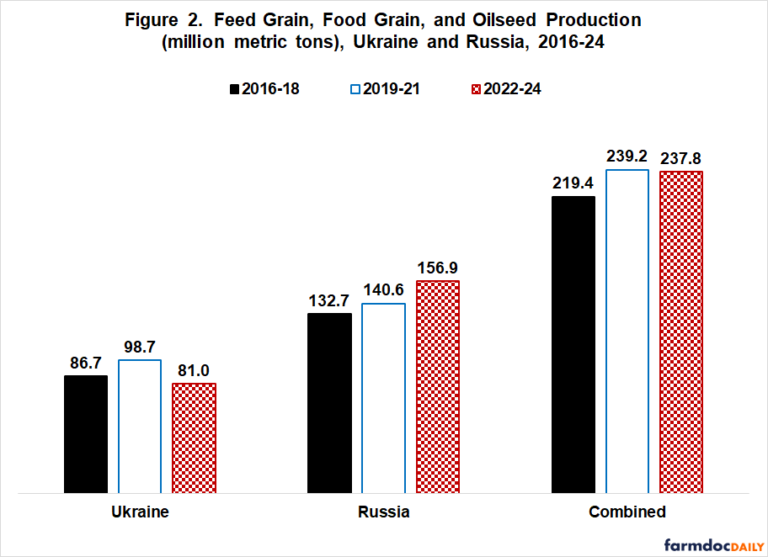

Farm Assets, Debt, and Interest Expense

Between 2012-2013 and 2023-2024, farm assets increased 52% as farm real estate (i.e. land and buildings) increased 59% (see Figure 2). Farm debt rose 73% as real estate debt rose 96%. Total and real estate interest expense increased even more (87% and 100%, respectively). Interest rates were higher in 2023-2024 than in 2012-2013. A 2-year average is used to smooth year-to-year variation.

Land Rent vs. Asset Cost

One indicator of the potential impact of crop safety net payments on land values is to compare the price of land to the rent farmers paid to crop the land. Using data from USDA, NASS (National Agricultural Statistical Service) surveys, per acre price of cropland was 52% higher in 2023-2024 than in 2012-2013 (see Figure 3). Cash land rent was 21% higher. The price to buy cropland clearly increased more than what farmers were willing to pay to crop it. Several factors could explain the difference, with crop safety net payments one of them.

Policy Implications

Policy needs to consider both the situation of individual farmers and the crop sector. To focus on one is to potentially create problems for the other.

The current economic picture of the US field crop sector is stark, even disturbing. Since 2013,

- price of US cropland increased 52%,

- as production of nine large acreage field crops incurred private market losses,

- more than offset by large crop safety net payments.

Value of cropland and other real assets are thought to be linked to returns they generate vs. alternative investments. To sustain the post-2013 increase in cropland price, private market return must increase, large safety net payments must continue, or interest rates, an alternative investment return, must decline (see November 26, 2024 farmdoc daily for a discussion of these three factors in the current cropland market).

Contemporary pressure for continuing, high crop safety net payments is evident in three ways. The ad hoc economic assistance of December 2024 is not far from the average annual safety net payments to the cost of production crops over 2014-2023 ($10 vs. $12 billion/year). The Farm Bill safety net debate has stressed the need to raise commodity program support levels and insurance premium subsidies. Additional ad hoc assistance is being touted should the tariff war cause US crop exports and prices to fall.

Pressure for more payments face an era of tighter Federal budgets, so they may not materialize. However, until they do not occur, markets will expect them to continue and price them into costs, such as land and machinery, in a process many economists describe as “capitalizing payments into future costs.”

More payments are thus unlikely to relieve the crop cost-price squeeze but instead raise the cost of producing crops.

In short, US crop agriculture confronts a government payment trap.

Unwinding this trap will unfortunately come with pain, such as higher financial stress and bankruptcies, unless higher prices or yields increase private market returns or interest rates decline.

The trap and its potential pain could largely have been avoided if past crop safety net payments had not exceeded private market losses. Limiting future total payments to no more than crop sector losses would be a first step in the unwinding and likely dampen the pain. More broadly, policymakers should always aim to avoid having total crop safety net payments exceed crop sector private market losses.

Source : illinois.edu