Divergent signals in Mexico

For much of this year, we have talked about Mexico buying less NFDM/SMP, a development that has driven U.S. suppliers to look elsewhere, especially to Southeast Asia. This trend abated in November with shipments of NFDM/SMP to Mexico posting the second highest month of the year behind only October, gaining 16% (+3,366 MT) over November 2019. It appears that powder demand, while still not consistently back to pre-covid levels may be on the road to recovery with an improved fourth quarter.

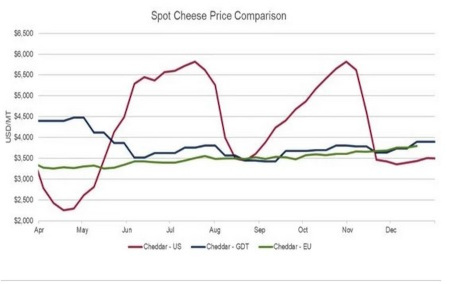

On the flip side, exports of cheese to Mexico weakened significantly. Reduced consumer demand inside of Mexico due to the COVID-19 pandemic and its severe economic consequences likely contributed to November’s 38% decline (-3,356 MT) in cheese exports to Mexico. The bigger factor was probably U.S. prices incentivizing international buyers to delay purchases over the summer and fall when domestic spot prices kept breaking records and cheese production was short compared to retail and food box demand. Still, despite the pandemic YTD cheese volumes to Mexico remain close to prior year levels, down just 1%.

Looking ahead, more affordable U.S. cheese towards the end of 2020 should have been the signal for international buyers, particularly in Mexico, to buy U.S. product. As a result, exports should rebound, but with more price volatility on the way, volatility in export volumes may follow.

Non-fat dry milk/skim milk powder sales to Southeast Asia slow in November

Let’s start off with some context. Through November, U.S. NFDM/SMP exports to Southeast Asia were up 50% compared to the same period last year – growth of more than 100,000 MT in 11 months. That acceleration was due primarily to a change in market share as the U.S. went accounting from 31% of total Southeast Asian NFDM/SMP trade in 2019 to 46% on an annualized basis. So, overall trade to the region is still very strong in 2020 despite November’s figures.

Still, NFDM/SMP exports to Southeast Asia in November represented a slowdown in the pace we have become accustomed to. Exports to the six major markets of the region (Indonesia, Malaysia, Philippines, Singapore, Thailand and Vietnam) dropped 27% (-7,399 MT). Shipments to Indonesia grew by 22% (+1,597 MT), but exports to the other destinations declined. Vietnam declined the most (-2,885 MT) followed by the Philippines (-2,686 MT), Malaysia (-2,314 MT), and Thailand (-1,099 MT).

The question remains “Why?” and “Should we expect this to persist?”

As to why – there were likely multiple factors all at play. A 46% share of trade for any supplier is well above the norm in such a highly competitive region with European, New Zealand and Australian suppliers all focused on gaining business. Thus, some regression in market share or volumes was to be expected.

Click here to see more...