By Kenny Burdine

In a lot of ways, 2021 was another frustrating year for cattle producers. Prices did improve this year for fed cattle, feeder cattle, and calf markets, but by relatively moderate amounts on an annual basis. When compared to price improvement for other commodities, cattle markets seem to have been a bit late to the party. Not to mention that CFAP payments offset some of the price regression in 2020 and similar payments were not available for 2021. While forage was relatively abundant in my area this year, some regions are the US are dealing with significant drought. And, it’s hard to grasp the damage done by the massive tornados of last weekend in much of the South, including my home state. Finally, changes in feed prices (and other inputs) have driven up production costs and impacted the value of feeder cattle and calves. Still, as I think about the future direction of cattle prices, I think that 2021 is likely going to be remembered as a year of transition.

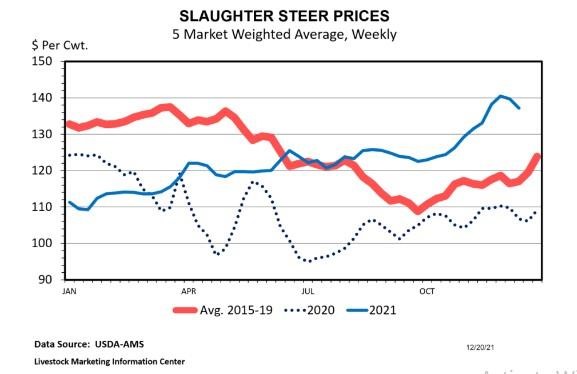

It appears that we turned the corner on fed cattle supply and beef production this year. While beef cow inventory peaked in 2018, 2021 will actually end up being the peak in beef production due to the normal time lag of beef production and the supply impacts of COVID in 2020. Feedlots appeared to get much more current with marketings by fall and fed cattle prices rose sharply in the 4th quarter. Since beef cow inventory has continued to decline and calf crops have continued to get smaller, tighter supplies should continue to support fed cattle prices going forward.