Soybean production is also projected higher at 4.3 billion bushels (up from the August projection of 4.29 billion bushels), reflecting expanded acreage that more than offsets lower yields in some regions.

However, USDA lowered projected export demand by 20 million bushels to 1.68 billion bushels, signaling continued challenges for international competitiveness. The result is a modest increase in expected ending stocks, adding to overall supply pressure.

Normally, the October WASDE would have provided the next update on crop projections and demand adjustments, but with federal government funding uncertain, that report was not released as scheduled. This pause in data will leave farmers and markets without USDA’s monthly benchmark during a critical point in harvest.

Heavy Carryover Persists Across Grains

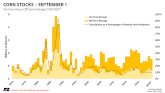

While corn and soybean inventories have eased compared to last year, they remain historically large. As of Sept. 1, corn stocks totaled 1.52 billion bushels, down 13% from 2024. Corn stored on farms was 640 million bushels, down 18% from a year ago, while off-farm stocks totaled 880 million bushels, down 10%.

Soybean stocks were estimated at 315 million bushels, down 8% from last year. On-farm soybean stocks totaled 92 million bushels, down 18%, and off-farm stocks were 223 million bushels, down 3%.

Wheat moved in the opposite direction. Total wheat stocks were estimated at 2.12 billion bushels, up 6% from 2024. On-farm wheat stocks were 690 million bushels, up 4%, while off-farm stocks reached 1.43 billion bushels, up 7%. USDA also revised 2024 production upward by 25 million bushels for corn and 7.7 million bushels for soybeans, slightly increasing residual supply.

Click here to see more...