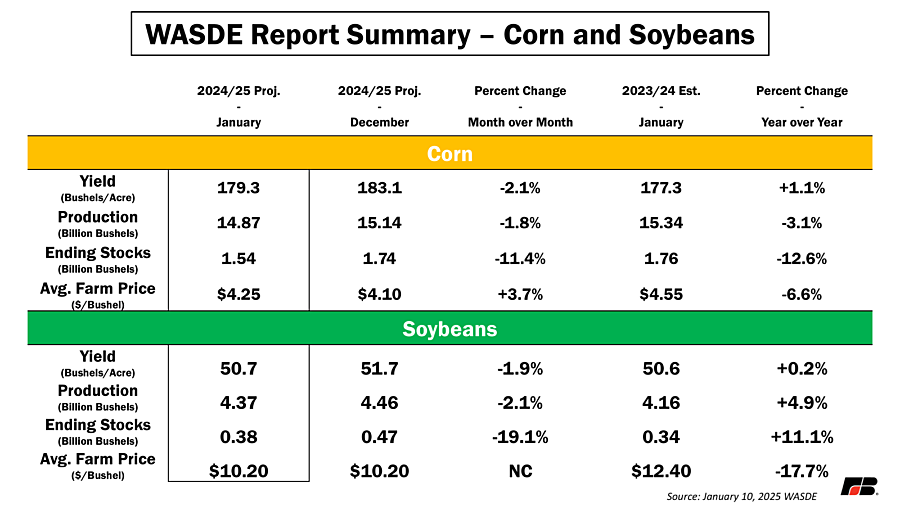

The most attention-grabbing news of the day was steep reduction in yield projections for marketing year 2024/25 corn and soybeans, falling by 2.1% and 1.9%, respectively, from December projections. These declines in yields led to declines in production, which when accompanied by only minor adjustments to consumption, are indicative of tightening supplies. Both corn’s and soybean’s drops in yields, and production, were below industry expectations, leading to increased prices in the futures markets for both crops.

When compared to the last time corn yields were updated in November, the sharpest declines at the state level were in Kansas (-6.5%), Indiana (-5.3%) and Minnesota (-4.9%). Despite a now year-over-year reduction in corn production of 474 million bushels (-3%), and projections for lower year-over-year ending stocks (223 million bushels, -12.6%), grain stocks as of Dec. 1, 2024, are down only 1% compared to 2023.

Soybeans followed a similar trajectory to corn. As compared to November reports, the decline in soybean yields was largest in Kansas (-7.9%), Tennessee (-6.7%) and Indiana (-4.8%). Domestically, reductions in soybean production combined with a marginal increase in domestic use led to a 19.1% decrease in projected ending stocks. While domestically ending stocks are tightening significantly as compared to December projections, global projected ending stocks had a smaller change of only 2.7%. Zooming out to a year-over-year look, soybean supply is still looser than the previous year with ending stocks increasing by 38 million bushels (11.1%) domestically and 719 million bushels (17.3%) globally. Grain stocks as of Dec. 1, 2024, were up 3% compared to 2023, led by an on-farm stocks increase of 6%.

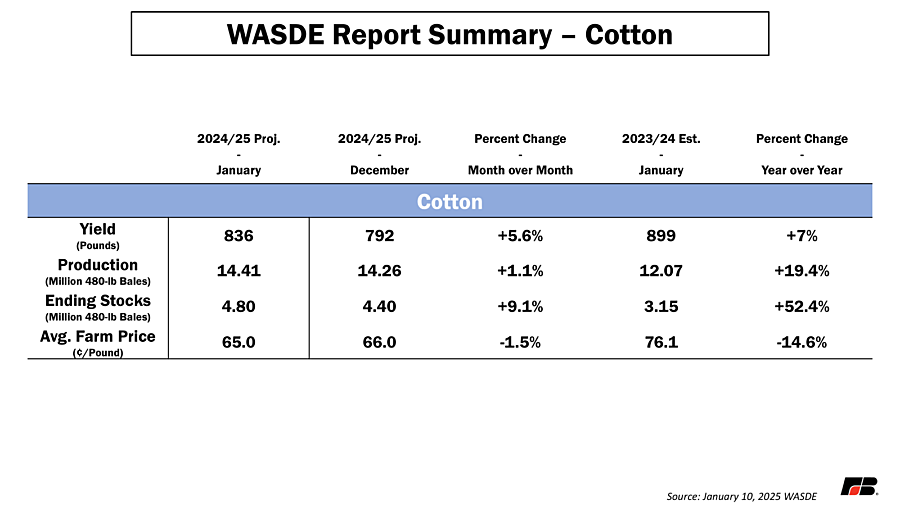

2. Bad Day for Cotton

This report did not contain good news for cotton producers. A slight increase in estimated production projections due to increased yields combined with a decline in exports of 30 million 480-pound bales (2.7%) caused ending stocks to increase by 9%. Notably, the decline in U.S. exports of 30 million bales perfectly matched an increase of Brazilian cotton exports, highlighting that the 2024 crop year will be the second where Brazil has displaced the U.S. as the world’s top cotton exporter.

Basically, production bounced back this year, in large part due to better growing conditions in Texas, but demand has fallen. This led to a nearly 15% decrease in price since last year, and a further projected 1.5% decrease in price since the December report.

3. Winter Wheat Planting - Decreasing in Breadbasket, Increasing in Fringe States

Farmers are projected to have planted 34.1 million acres of winter wheat for the 2025/26 crop year, an increase of 725,000 acres nationally (+2.2%) over 2024. However, the increase in acres was not spread evenly across the country. In fact, Kansas and Oklahoma, the states ranking first and third in total planted acres, declined by 200,000 and 100,000 acres, respectively. South Dakota (70,000 acres, -8.1%) and Tennessee (30,000, -7.9%) had the largest declines in acres on a percentage basis.

Most of the increase in acres came from states in the Great Lakes region, West Coast, and Southeast. By acreage, Montana and Texas had the largest increase at 300,000 acres each. On a percentage basis, South Carolina (45,000 acres, 56.3%), Michigan (150,000 acres, 37.5%) and Alabama (40,000, 36.4%) had the largest increases. But they weren’t alone, a whopping eight states increased their planted acres of winter wheat by 15% or greater.

Click here to see more...