By Rob Hatchett

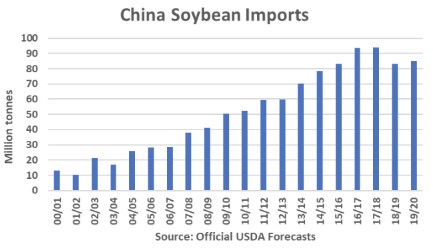

The U.S. Department of Agriculture’s (USDA) Foreign Agricultural Service (FAS) Post in Beijing issued its latest Oilseeds and Products Update in late October. In the report, the Post maintained its lower import forecast of 80.0 million tonnes in the current 2019/20 marketing year compared with USDA’s official October World Agricultural Supply and Demand Estimate (WASDE) of 85.0 million tonnes. However, the Chinese government and some industry officials are more bullish on soybean meal demand with forecasts for soybean imports seen between 84 and 89 million tonnes. If the Post forecast holds true, these would be the smallest soybean imports since 78.350 million tonnes were received in 2014/15. The following chart highlights the recent setback in China’s soybean imports from all locations that began in the 2018/19 marketing year coinciding with the deadly outbreak of the African swine fever (ASF) virus.

Estimates of the impact that the disease has had on China’s pig population are varied depending on the source, but the Post notes official estimates from China’s Ministry of Agriculture and Rural Affairs (MARA) pegged losses to sow and hog inventories at 39 and 41 percent, respectively. Skyrocketing Chinese pork prices have brought sharply higher margins to domestic operations that have continued their operations, and also have spurred greater imports of frozen meat in recent months. The following chart compiled by the Post of prices from consultants at JCI China shows estimated monthly average hog profits that have been growing at an increasing rate since July, most recently reaching around 2,400 Ren Min Bi (RMB)/head in mid-October. With domestic pork output unable to meet demand, China has turned to fill its protein void from the import market and through other alternative protein sources.