The financial figures are for the twelve-month period ending January 31, 2020. Because the year for evaluation runs from February 1, 2019 through January 31, 2020, this will differ from the 2019 tax return or year-end financial records for 2019. These figures can be calculated using your accounting records for that twelve-month from February 1, 2019 through January 31, 2020.

Applicants must declare other sources of compensation that they have received as a result of the disaster in the form of a dollar amount and brief description. For EIDL applicants who received a PPP loan, the dollar amount should be included along with a description indicating that is for a PPP loan. For EIDL applicants who have an outstanding PPP application, a note indicating PPP application and pending status should be included.

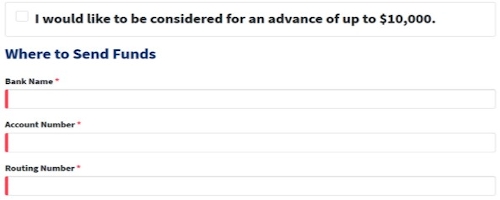

Application for the emergency advance is made as part of the traditional EIDL loan application. There is no way to apply for the emergency advance without applying for the traditional EIDL loan. The traditional EIDL loan application includes a check box that must be marked to be considered for the emergency advance. Applicants will be prompted to enter bank name, account number, and routing number.

In effort to get funds to businesses during the potentially slow loan review process, emergency advance funds are to be paid via direct deposit within three days of the application. However, numerous reports indicate that some businesses have waited up to a few weeks to receive the advance as the system was overwhelmed with applications. Finally, those applying for the traditional EIDL loan may receive and keep the emergency advance even if the traditional EIDL loan application is not approved. If approved for a traditional EIDL loan, applicants are under no obligation to accept a loan; farmers may receive and keep the emergency advance without accepting the loan.

EIDL General Information

The maximum loan amount for a traditional EIDL loan was initially $2 million per business, but recently lowered by SBA to a maximum of $150,000 per business. Program eligibility and loan amount dependent upon the size, type of business, and financial resources. The traditional EIDL loan is not forgivable and at this time only the emergency advance portion can be forgiven. The maximum loan term is 30 years, with repayment period and monthly payments dependent on the applicant’s financial conditions. The first monthly payment is automatically deferred for twelve months, although interest does accrue during this period.

For businesses impacted by Covid-19, the statutory 4% interest rate for traditional EIDL loans is lowered to 3.75% for small businesses and 2.75% for nonprofits. Loan terms may extend up to 30 years. Through the CARES Acts, the personal guarantee requirement is waived for EIDL loans of $200,000 or lower from January 31, 2020 through December 31, 2020. However, the maximum unsecured loan amount is $25,000, at which point traditional collateral requirements apply.

The primary criteria used to determine loan approval is a credit check indicating an acceptable credit history and deemed ability to repay the SBA loan.

Funds for both the traditional EIDL loan and the emergency advance can be used to pay fixed business debts, payroll, accounts payable, or other bills that could have been paid had the disaster not occurred. Generally, the following are not acceptable uses of funds from the traditional EIDL loan or the emergency advance: provide dividends, bonuses, or owner disbursements, repayment of stockholder loans, repair assets or acquire additional assets, refinance long-term debt, or relocate. Farmers should also note that no funds received through the EIDL program can be used to pay other loans owned by SBA or another Federal agency, which would include USDA loans administered through Farm Service Agency (FSA).

Funding Considerations

Borrowers who received a PPP loan (see farmdocdaily April 14, 2020) can apply for a traditional EIDL loan and associated emergency advance assistance, and vice-versa. However, the interaction between funding from the two programs is not clear. There is some overlap in approved uses for PPP loan funds and the traditional EIDL loan (and emergency advance) funds. For farmers who have received a forgivable PPP loan it is unclear if the EIDL emergency advance delivers additional forgivable funding provided it is used for a different set of eligible uses, or if the EIDL emergency advance would reduce the forgivable portion of the PPP loan. For example, consider a farm that received a $15,000 PPP loan and uses the full amount on payroll expenses in the approved eight-week time period. The farm has three employees and receives a $3,000 EIDL emergency advance which is used to pay approved rental expenses. The two sets of funds – PPP loan and EIDL emergency advance – were used on separate sets of eligible uses. At this time, it is unclear if the farm can receive the full $15,000 of forgiveness for PPP or if that loan forgiveness amount would be reduced by the $3,000 EIDL emergency advance. For businesses with existing EIDL loans originated prior to April 3,2020, PPP loans can be used to refinance EIDL loans made between January 31, 2020 and April 3, 2020. But current guidance does not provide specific instructions in situations where the traditional EIDL loan is obtained after a PPP loan, or when both are obtained after April 3, 2020, or when a traditional EIDL loan is not approved or accepted but emergency advance funds are received.

Conclusion

SBA has limited the traditional EIDL loan program and corresponding emergency advance assistance to farmers and eligible agricultural businesses to provide relief during the Covid-19 pandemic and in response to changes recently enacted by Congress. Farmers may apply now for the traditional, low interest EIDL loans, and corresponding emergency advance through a single application. Although the traditional EIDL loans are not forgivable at this time, the emergency advance of up to $10,000 per business, limited to $1,000 per employee, is forgivable when used for eligible purposes. Farmers may receive the emergency advance with no obligation to accept a loan offer. The interaction between PPP loan funds and the traditional EIDL loan and EIDL emergency advance proceeds remains unclear. Farmers receiving any funds from both programs are advised to utilize funds for separate sets of eligible uses and keep documentation while waiting on additional guidance.

Source : illinois.edu