Figure 1. December 2021 cotton futures prices.

Investors trade commodity futures along with stocks and bonds by taking positions on whether prices will increase or decrease, and the recent market fluctuations in the cotton-futures market reflect this increased activity. A large uptick in the net purchases of cotton futures (5,000 per day increase) led to the higher prices. Since, speculative purchases drove the cotton-price increase, the market may continue to remain volatile, and could be difficult to predict short-term.

Cotton Outlook

Although the recent uptick in prices has not been driven by fundamentals, the cotton market is in a good position for producers. The U.S. cotton harvest is underway, as 45% of acres nationwide (35% in Alabama) have been harvested as of October 31. It is looking to be a good cotton crop, with 64% of U.S. cotton acres rated as good or excellent condition compared to just 40% in 2020. Whether this translates to high yields will soon be determined. Cotton yields are projected to be greater than in 2020 across the U.S., with Tennessee being the only top-producing cotton state expected to see a decrease (shown in the table below). Nationwide cotton yields are forecast to reach 865 lb/ac, which would be the highest mark since 2018. Yields in Alabama are projected to reach 906 lb/ac, which would be a 14.7% increase from last year.

Table 1. Average Cotton Yields

Another factor impacting this year’s production will be the abandonment rate. The USDA estimates that 88.7% of planted acres will be harvested, after only 68.5% of 2020 planted acres were harvested. Combining the expected decreased abandonment with the high yields, 2021 production is projected at 17.65 million bales, up from 14.06 million bales in 2020. Alabama is forecasted to see a 2.9% increase up to 755 thousand bales.

Cotton demand is projected to match the strong production this marketing year (which began August 1, 2021). Overall, cotton stocks are expected to remain at the same level as they were when the marketing year began, at 3.2 million bales. U.S. cotton stocks reached their lowest point since 2016 at the start of this marketing year. The marketing-year average price forecast for 2021/2022 increased by $0.06 from the September estimate, to $0.90/lb in the U.S. The $0.90/lb figure would be the highest price ever for any marketing year and 35.7% higher than the $66.3/lb estimated for 2020/2021.

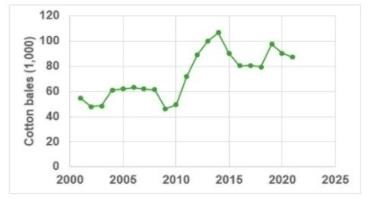

Globally, cotton stocks are projected to reach their lowest mark in three years, at 87 million bales (shown in Figure 2 below). This is due to higher predicted mill use in 2021/2022, up 3% from the previous marketing year. The leading cotton consumers are expected to increase or maintain their consumption levels this year, with cotton demand expected to increase in 2021/2022 in India, Pakistan, Bangladesh, Turkey, and remain constant in China. Global production is expected to be 7% higher in 2021/2022 than in 2020/2021, but the high consumption is still expected to allow global stocks to decrease.

Summary

Although the high recent cotton prices were driven by speculation, the fundamentals of the cotton market both domestically and globally remain strong for producers, with US stocks projected to stay among their lowest levels this decade and global stocks at a three-year low. The low stocks combined with sustained demand is a good signal for high cotton prices next year.

Global cotton stocks by marketing year.

Source : aces.edu