and Brenna Ellison

Department of Agricultural Economics

Purdue University

Last week we discussed the latest wave of responses to the Gardner Food and Agricultural Policy Survey by highlighting respondents perspectives on the extreme weather events this summer (farmdoc daily, September 20, 2023). This week’s article follows with a closer look at the alignment between those perspectives and federal agricultural policy.

Background

The Gardner Food and Agricultural Survey operates through quarterly panels of 1,000 U.S. consumers who volunteer for the survey and respond online. The panels are designed to be representative of the broader U.S. in terms of gender, age, census region, and annual household incomes (farmdoc daily, September 11, 2023). In last week’s post, we explored how the extreme weather events of the summer had impacted participants, as well as the impacts on policy perspectives. The discussion below builds on the responses illustrated in Figure 3 of last week’s post as to the preferences for government policy spending on responding to climate change and extreme weather. We noted the significant ideological and partisan differences, as well as some of the similarities.

Discussion

Congressional efforts to reauthorize the Farm Bill in 2023 are currently stalled. The negotiations are a victim of the impasse in the House of Representatives to fund the federal government in the next fiscal year, which begins October 1, 2023 (Hulse, September 23, 2023; see also, farmdoc daily, September 21, 2023). Farm bill negotiations are also stuck over directions in farm policy, most notably disagreements about the historic investments in conservation practices through the Inflation Reduction Act of 2022 versus offsetting the Congressional Budget Office projections—although not necessarily actual spending or payments to farmers—for increasing farm payment reference prices (farmdoc daily, September 14, 2023).

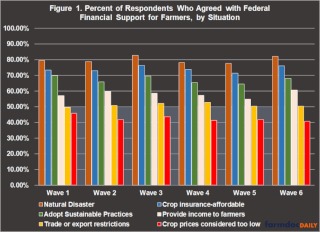

Farming has always required managing the risks of weather and the recent extreme weather across the Nation has provided very vivid examples. One justification for public policies that help farmers is to respond to these uncontrollable weather events and help farm production navigate the impacts of the unknown. Figure 1 tracks the responses from participants in the survey over the six waves dating back to May 2022. The responses illustrated in Figure 1 are for those participants who indicated in a previous question that they agreed the federal government should provide some assistance to farmers. In other words, these are the priorities of those who think the federal policy should pay farmers.

Over the past six waves of the Gardner Food and Agricultural Policy Survey (May 2022-August 2023), participants have consistently prioritized payments following natural disasters above other types of federal support to farmers (averages 80%). Similarly, participants have prioritized policies that make crop insurance more affordable (averages 74%). Crop insurance is the primary policy for helping farmers manage the risks from weather’s impacts on crops and it is subsidized by the U.S. government; on crop insurance, therefore, the Gardner survey finds relatively strong alignment with existing policy. USDA and Congress will often also provide payments to farmers following significant natural disasters – including wildfires, hurricanes, floods, excessive heath, winter storms, smoke exposure, drought, etc. Here again, the policy tends to align relatively closely with the public’s priorities.

One challenge for the currently stalled farm bill debate is the much lower support for policies that trigger payments to farmers when crop prices are considered too low (averages 43%). The Gardner survey has consistently found that respondents rank this reason for federal payments the lowest, and that it has never received more than 50% support from those who support federal assistance to farmers. This could provide an important perspective to the policy debate and possibly even serve as a warning to those who have prioritized the price-based payments over all other policies.

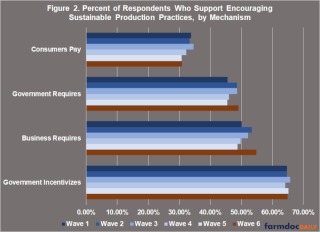

To add further context to the priorities from consumers, Figure 2 presents the percentage of participants in each wave who supported each policy mechanism for assisting farmers in the adoption of sustainable food production practices. Direct government incentives to the farmers have been the most popular policy mechanism across all waves (averaging 65%). Notably in the most recent wave, we find increases in both versions of mandatory mechanisms or requirements on farmers. First, support for business requirements on farmers increased to nearly 55% in wave 6 after averaging 51% in the previous five waves. Second, support for government requirements increased to just over 49% in wave 6, compared to under 47% in the previous five waves. Both responses received the highest support in the most recent survey and will be an issue watched closely in future surveys.

Also of note, we compared these results across those who said they were directly affected by extreme weather in the summer of 2023 (68.6% of sample) and those who were not (31.4% of sample). Those with direct experience were much more likely to support payments to encourage farmers to adopt sustainable production practices compared to those who did not (71.8% vs. 59.6%). They were also somewhat more likely to support making crop insurance protection more affordable (78.2% vs. 71.9%). Both groups had similar levels of support for payments following natural disasters (83.0% vs. 80.5%). Importantly, these differences are not causal, as those who are more likely to be impacted by extreme weather may also differ in other ways likely to influence these perceptions.

Concluding Thoughts

Current impasses in Congress include reauthorizing a farm bill in 2023. It may also offer the opportunity to consider the perspectives from consumers about federal policies. The Gardner Food and Agricultural Policy Survey provides a window into these perspectives across more than a year of quarterly panels. For the farm bill debate, a critical question might be the degree to which the policy priorities in Congress are aligned—or maybe more importantly not aligned—with the policy priorities of the general public. First, we have consistently found strong alignment around crop insurance and other policies that help farmers manage the impacts of weather risks to production. Here the farm interest priorities and the public’s priorities, as represented in these surveys, are most aligned. By comparison, however, the public’s priorities are not well aligned with the continued demand by farm interests to increase the reference prices that trigger payments to farmers. The surveys have consistently found this to be the lowest priority.

The highest priority in these surveys after those addressing weather or natural disasters, including through crop insurance, is to assist farmers with the adoption of sustainable production practices. Support for this priority has averaged 68% across the six waves. At the same time, the surveys have found consistently higher support for government incentives than for other mechanisms such as business or government requirements (averages 65%); respondents indicate the lowest support for having consumers pay more for these practices. We may also be seeing a notable increase in support for business and government requirements on farmers, but this could be an outlier in wave 6 and will be watched closely.

Combined, the responses may present an important warning to Congressional farm bill negotiators. If Congress were to reduce the historic conservation investments from the Inflation Reduction Act, that would amount to cutting from a higher priority (e.g., paying farmers to adopt sustainable practices) to offset the project costs of the lowest priority (e.g., paying farmers when prices are considered too low). This misalignment could magnify the risks for federal farm policy and reduce public support. While not definitive, the perspectives from these survey responses may provide further reason to reevaluate the demand for higher reference prices.

Source : illinois.edu